April 18, 2024

| “… they think we shall see for the first time in a decade two years with back-to-back growth.” |

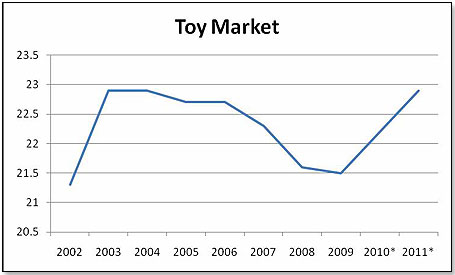

During this year’s Toy Fair and its aftermath, it became very clear that the buyers on my retail panel are taking a much more positive view of the U.S. toy market than they did a year ago. There are several reasons for this, but, in summary, they think we shall see for the first time in a decade two years with back-to-back growth. However, just to put this into perspective, even if they are right, the 2011 toy sales will, at best, equal toy sales in 2003.

During this year’s Toy Fair and its aftermath, it became very clear that the buyers on my retail panel are taking a much more positive view of the U.S. toy market than they did a year ago. There are several reasons for this, but, in summary, they think we shall see for the first time in a decade two years with back-to-back growth. However, just to put this into perspective, even if they are right, the 2011 toy sales will, at best, equal toy sales in 2003.|

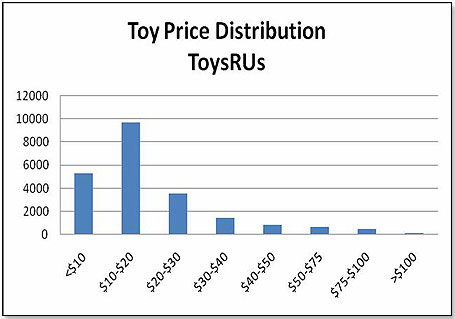

Price

|

SKUs

|

%

|

|

<$10

|

5,292

|

24.1

|

|

$10-$20

|

9,692

|

44.1

|

|

$20-$30

|

3,519

|

16.0

|

|

$30-$40

|

1,422

|

6.5

|

|

$40-$50

|

818

|

3.7

|

|

$50-$75

|

641

|

2.9

|

|

$75-$100

|

481

|

2.2

|

|

>$100

|

129

|

0.6

|

|

|

21,994

|

100.0

|

|

|

|

|

|

Movie Titles 2010

|

Release

|

Toy Licensee

|

Box Office

Last Movie*

|

Date Last

Movie

|

|

Avatar

|

12/27/09**

|

Mattel

|

None

|

None

|

|

How to Train Your Dragon

|

3/26/20

|

Spin Master

|

None

|

None

|

|

Iron Man 2

|

5/7/10

|

Hasbro

|

$228.6 M

|

2008

|

|

Prince of Persia: The Sands of Time |

5/28/10

|

Playmates/Vivid

|

None

|

None

|

|

The Last Airbender

|

7/2/10

|

Spin Master

|

None

|

None

|

|

Avatar [long version]

|

10/1/10

|

Mattel

|

$552.8 M

|

2009/10

|

|

Harry Potter and the Deathly Hollows: Part 1

|

11/19/10

|

Tomy/Neca

|

$294.2 M

|

2009

|

|

Tron Legacy

|

12/17/10

|

Spin Master

|

$33.0 M

|

1982

|

|

The Chronicles of Narnia: The Voyage of the Dawn Treader

|

12/17/10

|

Jakks Pacific

|

$135.5 M

|

2008

|

|

Movie Titles 2011

|

|

|

|

|

|

Thor

|

5/6/11

|

Hasbro

|

None

|

None

|

|

Green Lantern

|

6/17/11

|

Mattel

|

None

|

None

|

|

The Adventures of Tintin: The Secret of the Unicorn

|

6/23/11

|

|

None

|

None

|

|

Transformers 3

|

7/1/11

|

Hasbro

|

$393.7 M

|

2009

|

|

Pirates of the Caribbean 4: On Stranger Tides |

7/2011

|

No licensee at this point***

|

$301.7 M

|

2007

|

|

|

|

|

|

|

|

Harry Potter and the Deathly Hollows: Part 2

|

7/15/11

|

Tomy/Neca

|

$294.2 M

|

2009

|

|

The Hobbit

|

12/11

|

****

|

$345.5 M

|

2003

|

*U.S. only to Week 7 inclusive

**included in 2010 line-up as release date was after Christmas 2009

****Marvel’s Toy Biz had the license in 2003

|

Movie Titles 2010

|

Release

|

Toy Licensee

|

Box Office

Last Movie*

|

Date Last

Movie

|

|

|

Sorcerer’s Apprentice

|

5/16/10

|

None appointed

|

None

|

None

|

|

|

Shrek Forever After

|

5/21/10

|

Playmates/Vivid

|

$307.8 M

|

2007

|

|

|

Toy Story 3

|

6/18/10

|

Mattel/Thinkways

|

$245.6 M

|

1999

|

|

|

Movie Titles 2011

|

|

|

|

|

|

|

Jack the Giant Killer

|

2011

|

?

|

?

|

1962

|

|

|

Kung Fu Panda: The Kaboom of Doom

|

6/3/11

|

Mattel

|

$206.6 M

|

2008

|

|

|

Cars 2

|

6/24/11

|

Mattel

|

$220.0 M

|

2006

|

|

|

The Smurfs

|

7/29/11

|

Jakks Pacific

|

$11.2 M

|

1983

|

|

*U.S. only to Week 7 inclusive

|

Movie Titles 2010

|

Release

|

Toy Licensee

|

Box Office

Last Movie

|

Date Last

Movie

|

|

Alice in Wonderland |

3/5/10

|

Mattel

|

?

|

1951

|

|

Tangled [Rapunzel]

|

12/1/10

|

Mattel

|

None

|

None

|

|

Movie Titles 2011

|

|

|

|

|

|

Brave [The Bear and the Bow]

|

12/24/11

|

Mattel

|

None

|

None

|

*U.S. only to Week 7 inclusive

Copyright © 2024 TDmonthly®, a division of TOYDIRECTORY.com®,

Inc.